- The Real Problem Isn’t Workflow. It’s Interpretation.

- Where Coverage Breaks, and Why

- Coverage Intelligence: The Category Definition

- The Coverage Intelligence Formula

- What Coverage Intelligence Is Not

- Why Specialty Practices Carry the Highest Coverage Risk

- What a Coverage Intelligence Platform Does

- The Regulatory Moment

- Final Thoughts

Executive Summary

Coverage intelligence is the continuous interpretation and coordination of payer requirements, eligibility data, and clinical context to determine coverage accuracy before care is delivered. It operates upstream of billing, across three connected functions: payer eligibility verification, prior authorization management, and patient financial clearance. Its purpose is to resolve coverage ambiguity before that ambiguity becomes a denied claim, a delayed procedure, or an uncollected balance. For specialty practices, coverage intelligence is the layer that determines whether revenue is protected proactively or recovered reactively. Manta Health builds this layer.

The Real Problem Isn’t Workflow. It’s Interpretation.

Most practices approach coverage failures as process problems. The pattern is familiar: a denial happens, someone investigates the cause, a checklist gets updated, training is delivered, and the team moves on. The denial recurs three weeks later, hidden behind different conditions.

This cycle continues because the diagnosis is wrong. Eligibility errors, missed authorizations, and patient financial surprises do not persist because the process is broken. They persist because payer requirements are fragmented across portals and PDFs, the rules change without notice, and the same case can produce two different answers depending on which staff member reviews it. No checklist resolves that kind of ambiguity. No workflow tool, however well-configured, replaces the judgment required to interpret a payer policy that was rewritten last month and applies differently to a Medicare Advantage plan than to its commercial sibling.

The foundational claim of the coverage lifecycle is that revenue is lost upstream of the claim. The deeper claim is that what gets lost upstream is interpretation. Practices that solve for interpretation solve for revenue. Practices that solve for workflow solve for throughput, which keeps the same problems running faster.

Where Coverage Breaks, and Why

Three failure points account for the majority of preventable pre-service revenue loss.

Eligibility. Coverage is verified at intake, often through a clearinghouse or payer portal, and the response confirms that a plan is active. What the response does not confirm is whether the specific procedure is covered, whether the patient’s deductible has been met, whether a coordination of benefits issue is pending, or whether the plan changed in the last 30 days. Staff treat eligibility as resolved. The downstream denial says otherwise.

Prior authorization. AMA prior authorization surveys put the administrative cost at roughly $23,000 per physician per year, with 14 hours per physician per week consumed by PA work. Roughly 15 percent of claim denials trace back to missed or incomplete authorizations. The cause is rarely effort. It is documentation prepared against criteria the practice did not fully know at submission time, because the payer’s requirements were neither static nor centrally published.

Patient financial responsibility. Estimates are calculated manually, often inaccurately, and communicated late. The patient receives a balance after treatment, when their willingness and ability to pay are at their lowest point. Collections costs rise. Write-offs follow. The revenue was never genuinely protected. It was deferred and partially lost.

These three failures share a common cause, which is what the missing layer in the revenue cycle technology stack names directly. EHRs were built to document clinical care. Clearinghouses were built to transmit claims. Neither system was designed to interpret coverage. The gap between them is where coverage intelligence sits.

Coverage Intelligence: The Category Definition

Coverage intelligence is the system capability that interprets fragmented payer data, adapts to changing rules, and resolves coverage ambiguity before it produces a denial, a delay, or a write-off. It is continuous rather than episodic. It is interpretive rather than transactional. It operates across the full pre-service window, from scheduling through day-of-service validation, and it is embedded directly in clinical and billing workflows rather than running as a parallel administrative track.

The three operational functions covered by coverage intelligence are payer eligibility verification, prior authorization management, and patient financial clearance. These are sometimes mistaken for the category itself. They are not. They are the surfaces on which coverage intelligence acts. A practice that performs all three manually has not implemented coverage intelligence. A practice that runs three disconnected vendors for them has not implemented coverage intelligence either. The category describes an integrated capability that operates over all three, with interpretation as its core function.

Manta’s Coverage Intelligence glossary defines the full vocabulary of this emerging category, including the distinctions between coverage intelligence and the adjacent categories it is frequently confused with. The glossary explains the terminology. This blog makes the operational case for why the terminology matters.

The category is new. The capability it describes has been needed for as long as payer complexity has existed. What changed is that the volume, variability, and pace of payer rule changes finally exceeded what manual interpretation could absorb. The market is responding by naming the layer that was always missing.

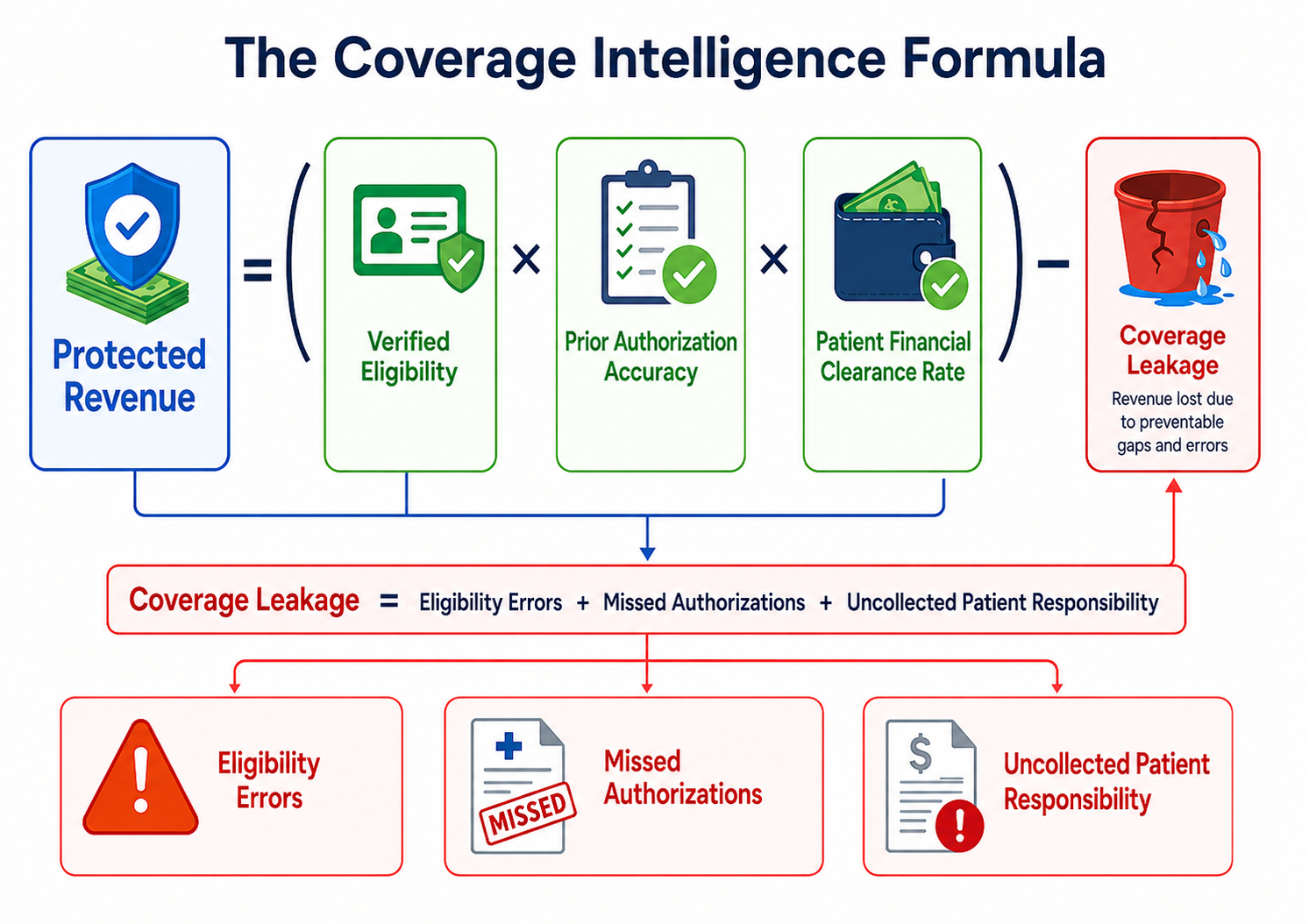

The Coverage Intelligence Formula

A useful way to make the category concrete is to express it as a relationship between variables.

Every variable in the protection equation is an interpretation problem. Verified eligibility depends on reading benefit data correctly for the specific procedure. Prior authorization accuracy depends on assembling documentation against payer-specific criteria. Patient financial clearance rate depends on calculating responsibility from those benefits in advance and securing payment before treatment. Coverage leakage accumulates wherever interpretation fails.

Anchored to the operational benchmarks, the leakage is not theoretical. $23,000 per physician per year on PA administration. 14 hours per physician per week. 15 percent of denials originating from missed authorizations. 10 percent of patients abandoning care due to PA delays. Each of those numbers is a coverage intelligence gap with a dollar figure attached.

What Coverage Intelligence Is Not

The category is most useful when its boundaries are visible. Three adjacent categories are commonly mistaken for coverage intelligence, and each handles a different problem.

Clearinghouses move data between providers and payers. They transmit eligibility requests, claims, and payer responses, including standard eligibility files such as the 271 response. Their role is to confirm that the transaction was sent, received, and returned. They generally do not determine what the response means for a specific procedure, plan, or patient. Coverage intelligence adds that layer of interpretation, helping practitioners understand what the payer response actually permits, requires, or leaves uncertain.

Revenue cycle management operates downstream of care delivery. It manages claims, denials, payment posting, and patient collections. RCM measures financial outcomes after the fact and works to improve them. Coverage intelligence influences those outcomes upstream, by preventing the failures that RCM would otherwise have to recover from.

Workflow automation executes defined tasks with stable inputs. It is effective where the rules do not change and the documents are predictable. Coverage intelligence operates in the opposite environment, where rules change frequently and the inputs are fragmented across sources. Automation runs faster. Coverage intelligence runs smarter.

These boundaries matter because the market has a history of collapsing new categories into existing buckets. Coverage intelligence is not a clearinghouse with AI features bolted on, and it is not RCM software repositioned. It is a different layer of the stack with a different job.

Why Specialty Practices Carry the Highest Coverage Risk

Coverage intelligence applies broadly. The acute need is concentrated in specialty procedural practices, including ophthalmology, GI, orthopedics, ENT, radiology, and ambulatory surgery centers.

These practices share four characteristics that amplify coverage risk. Procedure-driven revenue models mean that a single denied authorization has an outsized financial impact. High-frequency CPT workflows produce a steady volume of payer interactions that compounds error rates. Medicare and Medicare Advantage exposure brings documentation requirements that have historically been less standardized than commercial payer rules. And the procedural specialties carry some of the highest prior authorization volumes in ambulatory care.

The downstream effects are measurable. Roughly 10 percent of patients abandon care because of prior authorization delays, with 78 percent of physicians reporting this directly. The patterns of denial in retina-heavy ophthalmology are documented in decoding the denial, and the staff burden of authorizing a single anti-VEGF treatment is captured in the Eylea prior auth nightmare. Both pieces show how the absence of a coverage intelligence layer turns routine procedures into administrative bottlenecks.

For these practices, coverage intelligence is not an efficiency play. It is the operational difference between scaling procedural volume and watching it stall against an administrative ceiling.

What a Coverage Intelligence Platform Does

Operationally, a coverage intelligence platform runs four functions continuously and in coordination.

Real-time eligibility verification queries payer systems across more than 1,300 payers and returns benefit data interpreted for the specific procedure on the schedule. Where coverage is unknown or partial, insurance discovery surfaces active plans the practice was not aware of.

Prior authorization determination identifies whether authorization is required for a specific CPT code under a specific payer rule. Where authorization is required, the platform assembles the documentation against payer-specific criteria, submits through the appropriate channel, and tracks status. Where denials occur, agentic AI appeals are generated and submitted immediately, with overturn rates above 90 percent on appealable cases.

Patient financial clearance calculates patient responsibility from the verified benefits, generates an accurate estimate, communicates it before treatment, and supports pre-treatment payment collection via SMS, email, or in-clinic.

The defining characteristic of the platform layer is that these functions are not parallel tools running independently. They are coordinated by the same intelligence layer, with the output of eligibility verification flowing directly into authorization scoping, and the output of authorization flowing into patient estimate generation. The coordination is the product.

The Regulatory Moment

The regulatory environment is moving in coverage intelligence’s direction. CMS-0057-F, the 2027 Prior Authorization Rule, requires impacted payers to respond to prior authorization requests within 72 hours for urgent cases and seven days for standard requests. It also requires payers to build FHIR-based APIs, including Da Vinci PAS, to support electronic authorization workflows.

The regulation accelerates the timeline payers operate on. It does not, on its own, make practices ready to operationalize that acceleration. A 72-hour payer response window only delivers value to the practice if the practice can submit complete, payer-aligned documentation in the first place. A FHIR API only delivers value if the practice has a system capable of consuming it and acting on the response in real time. The introduction of Medicare prior authorization changes adds the same pressure to a payer category that historically had few authorization requirements at all.

Coverage intelligence is the practice-side capability that makes regulatory compliance executable. The regulation defines what payers must do. Coverage intelligence defines what practices need to be in place to convert faster payer responses into protected revenue.

Final Thoughts

Coverage intelligence is not a product category invented for marketing convenience. It describes a genuine capability gap that has always existed between clinical systems and billing operations, and that has become impossible for specialty practices to absorb manually. The term is emerging because the problem it names has reached a point where naming it accurately is the precondition for solving it.

Practices that treat coverage as an intelligence problem will protect more revenue, reduce administrative overhead, and scale procedural volume without scaling administrative headcount. Practices that continue to treat it as a workflow problem will keep optimizing the speed at which the same denials recur.

The category is new. The work it describes is not. This piece is one of the early records of the definition.

See how Manta’s Coverage Intelligence platform protects specialty practice revenue before care is delivered. Book a demo.

-cropped.svg)

.svg)